A report from Irish Life shows that the present average age for starting with a company pension plan is 37, with an average contribution of 11.4% between a person's savings and the employer contribution.

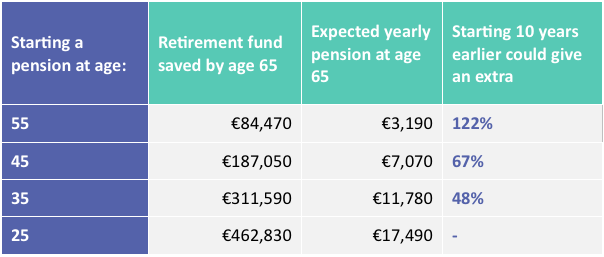

The figures come from a survey of the company’s members who are in defined contribution (DC) schemes, and the report concludes that if people joined just ten years sooner, their retirement income could be higher by anything from 50% to 120%.

The report looks at the main pensions issues — coverage (the number with pension plans) and adequacy (the amount people can expect based on the amount they are saving). A typical DC member was earning a salary of €51,250 and was contributing 11.4% of their salary to their scheme, including the employer contributions.

The result of that is that such a person is likely to receive only €13,249 per year (or just over 25% of their salary). The state pension stands at €12,650 annually, but the total of €25,900 is still just 50% of average salary, a considerable cut in income on retirement.

Pension providers are facing an uphill battle to persuade workers to start pension savings earlier, as Irish people are postponing significant life decisions, such as getting married, buying a home, and having children until well into their thirties.

In Association with

For example, the average age of marriage in 1977 was 25 years but, 40 years on, in 2017, the average marriage age was 35.

Corporate business managing director Tony Lawless said: “People are delaying big life decisions and enjoying their young-adult lives for longer. People are starting their DC pension at age 37, which might still seem young. But when it comes to pensions, the earlier people start the better.”

He quoted data from the report showing how starting contributions earlier can boost retirement income substantially. For example, joining a company plan at 25 could add almost 50% to their income level as compared to 35, based on certain assumptions with regard to tax relief, pay increases (average 2% annually), investment growth (4%) and interest rates (average 2%).

Lawless added: “The biggest challenge is making pensions more appealing; our research found that 29% of people say they just never got around to starting a pension.”

Lawless is in favour of automatic opt-in in schemes in the face of this. “People need help and encouragement to get started with pensions — being automatically enrolled into a pension by an employer or by the government represents a big nudge," he maintained. It removes the need to make a pension decision at an individual level, which turns pension inertia into a positive.

“Those who are auto-enrolled into a pension will see major benefits in the long run. Once people are signed up, it’s about helping them understand what level of pension they can expect at retirement and helping them to take control of that. We need to make it easier for people to take smarter steps for better outcomes at retirement.”